Table of Content

While VA home loans come with affordable monthly payments, there are ways to reduce them further. ARM might be a good option if you can afford the monthly payments, even if they increase. Moreover, it can be a wise choice if a decrease in interest rates is anticipated. Candidates who make a downpayment of less than 5% are expected to pay 2.3% of the total loan amount if they are borrowing a VA loan for the first time. For every subsequent use, the funding fee is 3.6% of the total loan amount. Several factors could affect the monthly payments as shown on a VA calculator.

By the time everything is said and done, though, they can increase a borrower's expenses by a considerable margin. As noted previously, the interest rates for VA home loans are generally quite a bit lower than for traditional mortgage products. In fact, this is one of their major selling points and is the main reason why so many people are sold on them.

Loan origination fee

Lenders will usually require the purchase of the lender’s title insurance, which only protects their interest in the property. You should strongly consider paying the one-time fee for the owner’s title insurance to ensure you’re covered as well. Instead, VA borrowers pay a one-time funding fee that helps pay for all the great benefits the VA program provides. It's not unusual for buyers to work with their agents to negotiate for sellers to pay certain closing costs. Buyers can ask the seller outright to pay these costs and fees from the sale proceeds.

Below is a summary of the inputs and calculations used to calculate estimated payments and closing costs. Depending on your situation, you may decide to purchase optional discount points, opt for a home inspection or owe additional homeowners association dues. If you’re using a VA home loan to buy, build, improve, or repair a home or to refinance a mortgage, you’ll need to pay the VA funding fee unless you meet certain requirements. When you're planning to get a VA loan, be sure to factor closing costs into the equation. That said, they may not all fall on you; there are ways you can potentially avoid having to pay some of these fees. Closing costs typically end up falling somewhere between 3% and 5% of the total loan amount.

Navy Federal Investment Services

Once a lender has that application in hand, they’re legally required to send you some key documents and disclosures within three business days. Each point you buy at closing costs 1% of your total loan amount and will reduce your interest rate by 0.25%. One important thing to note is that discount points must be paid for by the buyer and can’t be covered by seller concessions.

Besides negotiating with the seller to pay for some of the closing costs, you can cut your expenses by avoiding points, which reduce your interest rate but cost money upfront. Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories.

You’re signed up

A seller can contribute up to 4% of the loan amount on a VA loan. The home seller can agree to pay a portion of the buyer’s closing costs, up to 4 percent of the mortgage, including the funding fee or origination fee. Note that for a VA loan, sellers are always required to pay for the real estate agent commissions, any brokerage fees and for a termite report. Some veterans with a service-related disability may be exempt. The funding fee can be paid up front at closing or financed into your loan.

If your down payment is less than 20%, most lenders will require you to pay mortgage insurance. Bank of America offers several options to help lower your down payment or other closing costs. Connect with a lending specialist or learn more about programs offered by Bank of America. So, even though VA closing costs can take a chunk out of your savings, Clever can help you get some of that right back into your pocket. It’s a one-time fee, and the amount depends on how much you’re putting down and whether or not you’ve used the VA loan program before.

In this way, you could incur some extra expenses when trying to secure a VA home loan. Although they vary depending on where you live in the country, there are limits on how large of a VA home loan you can take out. Those who are looking to purchase a very expensive home, for instance, may be discouraged by the loan limits that are imposed by the VA home loan program. If the home that you want to buy exceeds the loan limits set by the VA home loan program, you will have to finance the balance through another mortgage program. This can seriously negate the benefits of using the VA home loan program. Still, the limit in most areas is currently $729,000; for the vast majority of people, that amount is more than enough for what they are looking at.

Here is a list of our partners and here's how we make money. Apply For A COE - Next, you're going to need to apply for a COE, or Certificate of Eligibility. You will need this certificate when you approach a VA-approved lender for a home loan.

This is optional, but it can save money if you keep the home loan long enough to benefit from the lower rate. Also, active duty service members who have received a Purple Heart won’t have to pay this fee. We’ll take a closer look at the various types of closing costs in the next section. The Loan Estimate offers a detailed picture of the loan’s estimated costs and fees along with some of its key features. State and local governments charge a fee to record your deed and mortgage-related documents. Some of your real estate transaction details will become public records, accessible to anyone in your community and beyond.

When settlement requires attorneys, their itemized charges are outlined in closing documents and passed to buyers for payment. The third tab shows current local mortgage rates to help you estimate payments and find a local lender. A guide to better understanding closing costs is published below the calculators. Our guide also lists state-by-state average closing costs before and after taxes. When you buy or refinance a home with a VA loan, you’ll be responsible for paying closing costs. These are fees paid to your lender for processing and finalizing the details of your loan.

It is simple to check whether the home is safe for living or not. Generally speaking, the best time to borrow a loan is when you know you can afford it. You might also want to spend some time on improving your credit score before applying so you can get the best quote.

If you are still unsure about whether or not you qualify, you should use the Veteran Affairs Eligibility Center to see what they have to say. Covering this base is important if you want to proceed with obtaining a VA home loan. The G.I. Bill of 1944 is where the VA Loan Guaranty Program originated. Considering that their lives were put on hold in many ways due to their military service, the bill was designed to give them a helping hand. The VA Loan Guaranty Program aimed to make housing affordable for returning GIs.

Who pays closing costs on a VA loan?

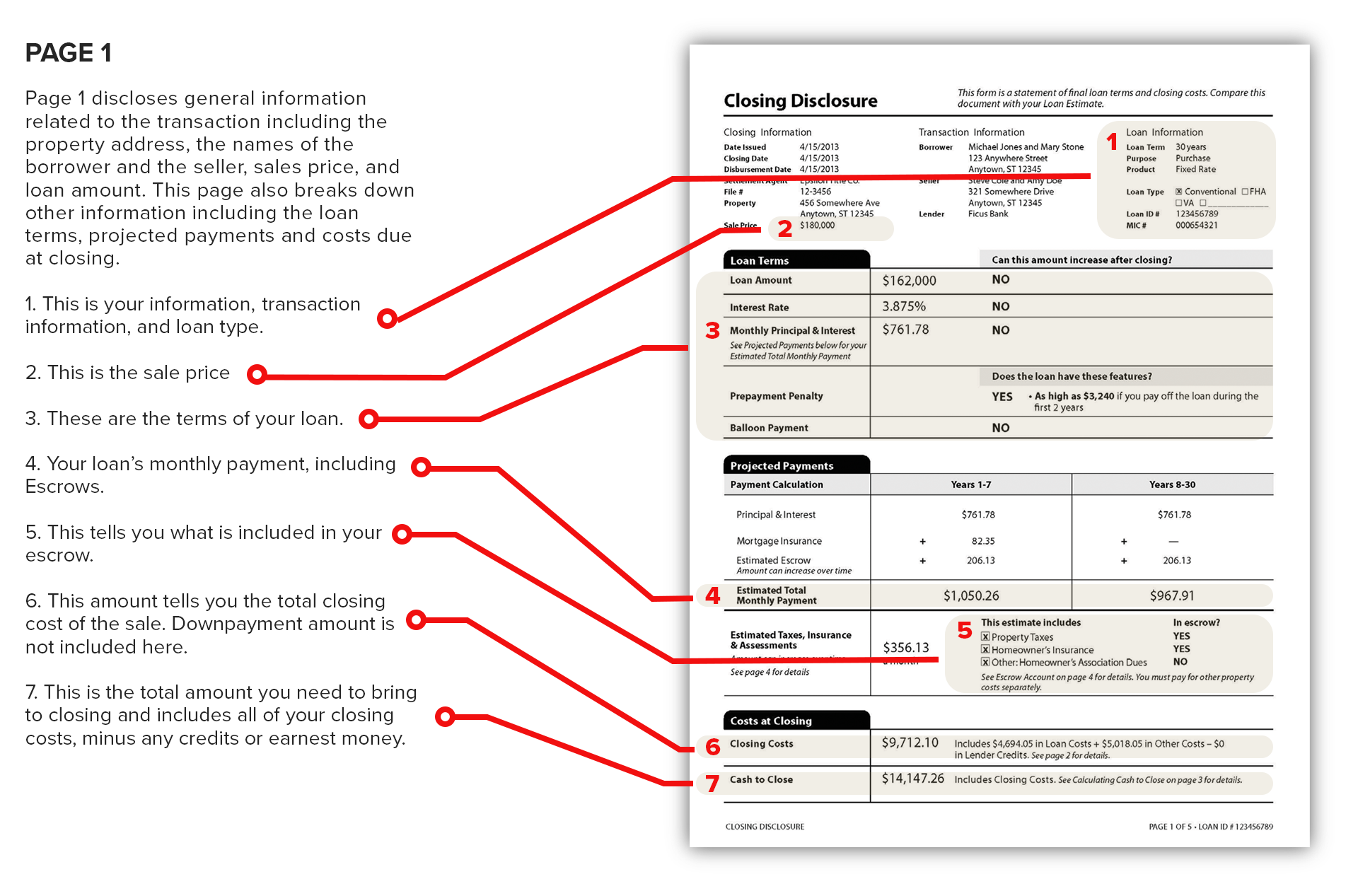

This estimate can give you confidence that you are prepared and have calculated closing costs correctly. Three business days before closing, you will then receive a Closing Disclosure with the final closing cost amount. Don't worry if this box is unchecked while you're shopping around — most lenders aren't going to lock in a rate if you haven't committed to the loan.

To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. You refinanced your VA loan into a non-VA loan and still own the home.

No comments:

Post a Comment